Welcome to the first ever newsletter from Crypto352.

We're really happy to be sharing this first edition with you, but we want to be clear up front that nothing here is financial advice, and you should always do your own research before acting on anything we write.

This newsletter is split into two parts.

The first part is an objective rundown of the events shaping financial markets right now, along with the data behind them and what we think the likely outcomes are.

The second part is more personal and reflects the opinions of the author, who may also share additional research, ideas, and trades based on those opinions.

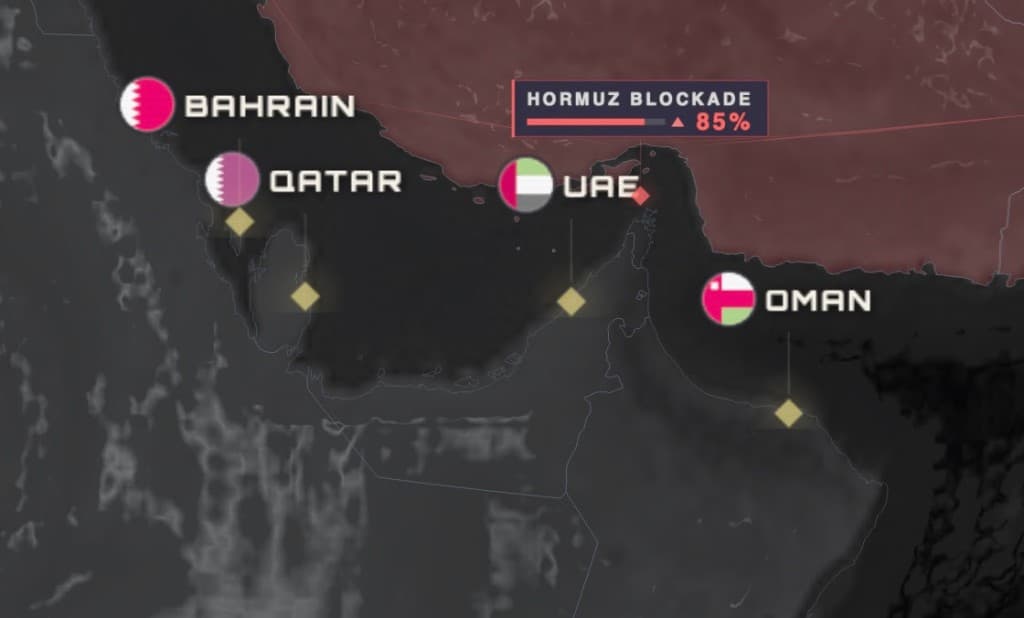

War

Let's talk about the Iran, Israel, and USA situation, since it's been impossible to avoid.

We won't go through every detail because you've probably already heard most of it.

What's interesting is that a dormant asset has woken up and is now reshaping how this conflict plays out across the Middle East.

That asset is the Strait of Hormuz, the 33km wide corridor that controls how oil flows in and out of the region.

A few years ago, most people looked at Iran as a weaker player, a country that was constantly pressured by Israel and the US.

Today, it's clear that Iran can shake global markets simply by threatening to close that passage of oil.

We saw exactly how much power that gives them when they actually went ahead and blocked the strait. Nasdaq, the S&P, crypto, and stocks all dropped sharply at once.

Trying to predict what happens next is genuinely difficult.

Crypto352 publicly flagged the start of this war a few weeks before the first attacks, and we also expected the strait to become a political weapon.

Where we got it wrong was assuming the Trump administration already had a plan to neutralize that threat.

That assumption didn't hold up, so this conflict has now moved into a stage of uncertainty that we don't think can be reliably predicted from where we sit.

We'd love to be able to call an ending and position around it, but the level of uncertainty right now is simply too high.

This war also carries history that runs much deeper than any deal involving economic assets could fix.

It touches on tradition, land that was taken, populations that were displaced, long held resentment, and political structures that have been entrenched for decades.

Before we move on from this topic, we also want to flag our concern about the Ukraine and Russia war.

We think this is heading toward either a full settlement or a much sharper escalation, possibly involving a NATO member directly. We'll keep watching this closely and update you as things develop.

Powell vs. Warsh: What the Fed Chairman Change Means

Powell has represented institutional independence at the Fed for years, and he's paid a political price for it.

Trump's nominee, Kevin Warsh, is widely seen as someone aligned with Trump's thinking, and his views give him both a reason and an intellectual basis to support rate cuts later this year if the data allows it.

Trump's New Approach: Loyalists Over Independents

Trump's experience with Powell, who refused to lower rates under pressure from the White House and pushed back publicly when the DOJ opened its investigation, has clearly shaped how Trump thinks about appointing technocrats going forward.

He now openly expects senior appointees to share his goals. He's said he would be disappointed if Warsh doesn't move quickly on cuts, and that Warsh wouldn't have been named as the likely chair without agreeing on the direction rates should take.

The message here is pretty simple. Warsh is expected to deliver on easing.

There Is Optimism for This Year

The first reason is that markets were already priced in the war and have moved past it. The S&P 500 has wiped out every loss tied to the Iran conflict and is sitting at record highs, even though the ceasefire remains fragile. That tells us the average buyer is focused on earnings and is operating under the assumption that this conflict won't structurally damage the economy. Several strategists have pointed out that war driven selloffs tend to be sharp but short, and this episode has followed that pattern almost exactly.

The second reason is that earnings and AI spending are carrying the market. AI related names and semiconductor stocks have surged since the March low, with semiconductor indices up over 30 percent, and the largest tech companies posting strong double digit gains for the year despite the oil shock. Hyperscalers are still planning to spend over 500 billion dollars on AI and data centers this year, with companies like TSMC and major cloud providers guiding for revenue growth above 30 percent. None of this suggests the war has slowed down the broader investment cycle.

The third reason is that strategist targets are still above where the market sits today. Major firms that updated their forecasts after the war began still see the S&P 500 ending the year roughly 6 percent higher than current levels, with European equities expected to do even better, around 10 percent. Their underlying view is that the damage from the Iran conflict is temporary rather than structural, and that the bigger risks lie in a potential oil spike or stress in private credit markets, not in equity valuations themselves.

The fourth reason involves the broader macro picture and the central bank. Even with oil prices higher, the shock from Iran hasn't pushed the economy into recession. Instead we're seeing inflation that's elevated but easing, growth that's softening, and a Fed that's closer to its first cut than its last hike. If Warsh leans into a story built around AI driven productivity and the economy normalizing after the war, that gives him room to justify a couple of cuts before the year ends. Markets aren't fully pricing that in yet, which means there's room for risk assets to react positively if it happens.

The fifth reason is that sentiment doesn't feel euphoric right now. We just went through a serious scare involving Iran, oil, and the Fed, yet the market is sitting at all time highs. Usually that combination means a lot of investors are still underweight or only reluctantly long, still climbing what people call the wall of worry. Flow data and commentary from strategists show buying concentrated in AI, quality growth names, and emerging markets, rather than everything across the board. That suggests there's still capital sitting on the sidelines if the war keeps fading as a market driver.

The Presidential Market Cycle Theory

This theory says that the second year of a presidency, which is where we are right now, tends to be when presidents start new conflicts or push through unpopular policies, since they still have two years before facing voters again. Historical data supports this.

The second year of a presidential term averages a market gain of around 3%, compared to 11% to 15% in the other years.

You can see this playing out right now. Trump started a war involving Iran, took action against the Venezuelan president, and rolled out a series of controversial policies all at once.

Kevin Warsh gives Trump a way to shift the narrative and give markets a temporary boost, but he won't be able to fix an actual recession on his own.

Yesterday's CPI print came in at 4.2 percent, which confirms inflation is running hotter and isn't great news for anyone hoping for quick rate cuts or a continued rally in risk assets.

Data like this will be covered separately in something we're calling the Data Day report, which will go out alongside the newsletter but as its own piece.

What Happens Next

Trump needs the market to look good heading into November, when the House vote takes place. Whoever controls the House controls how easily legislation and policy can move forward, so the stakes here are high.

For Trump, that means he needs voters feeling optimistic, and the most direct lever for that is lower interest rates. Cheaper borrowing pulls new money into the system, which tends to lift equities, crypto, and real estate all at once. As we've already covered, Trump isn't likely to appoint someone he expects to push back against that plan.

So our view is fairly straightforward. Once Warsh is confirmed, we expect him to move toward lower rates within the next few months, and we expect that move to be framed around AI driven growth, the end of the Iran conflict, and markets sitting at record highs.

Personal Note from the Author

Geopolitical tension has been a major part of my strategy since this Iran conflict began, and we built it directly into our trade setups, which gave us a very strong win rate during that period.

That edge is mostly gone now. Part of it is that the market has already priced in a lot of these scenarios and has become more resistant to shocks. The other part is what I mentioned earlier, which is that it's just not realistic to map out where this war goes from here.

The Fed chairman change is something I started preparing for about a year ago. We spent that time studying Warsh and the environment he's about to step into, and overall our read on it has held up well.

The Presidential Market Cycle Theory is something we follow closely, and based on it, we think this year ends up being a bottom.

Looking at Bitcoin and the fact that it's still down around 50 percent from its all time high, we're betting on new price discovery happening later this year and continuing into the following two years.

That's why I'm currently positioned long across the board, with no short positions on anything.

My current positions include Bitcoin, Solana, TON, Pump, AVAX, and ETH.

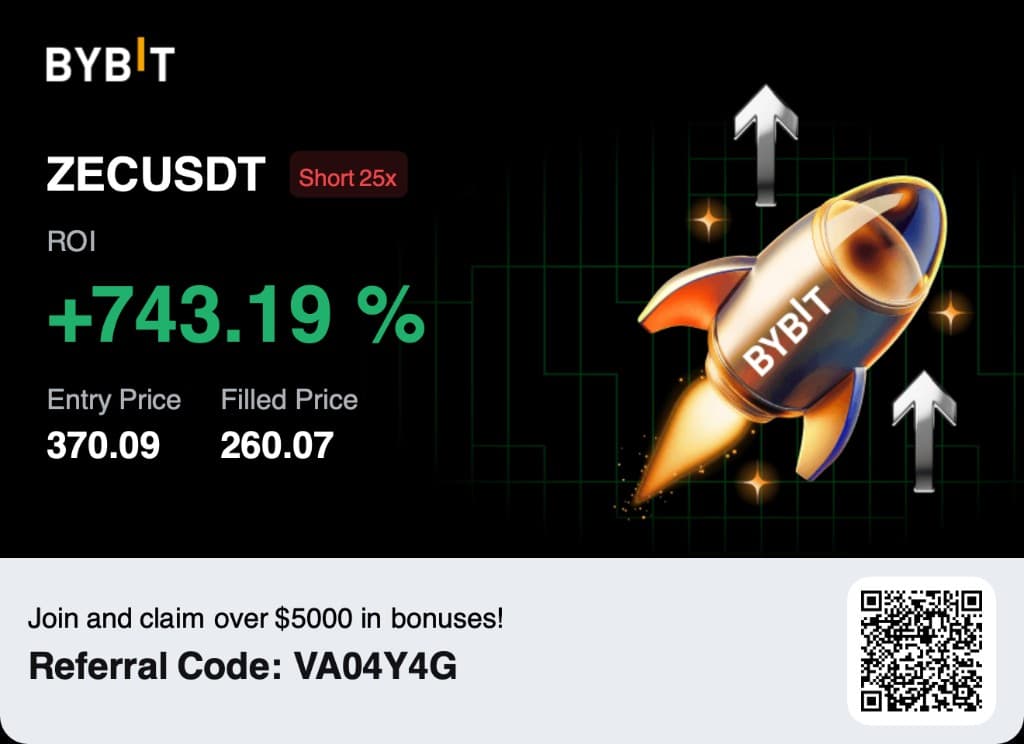

The one asset I'm interested in shorting is ZEC. On April 20th I posted an Instagram story saying I was shorting ZEC with real size, and a few days ago I closed that position with a solid profit.

The trigger for the drop was that a researcher working with Claude found a vulnerability in ZEC that could have allowed someone to mint an unlimited number of coins. What's interesting is that there's no way to verify whether anyone actually exploited it, since ZEC's privacy pool makes it impossible to trace the entry of new coins.

For me, that alone is reason enough to short this token down to zero, though I'll likely look to re-enter the short at higher prices if the opportunity comes back.

Below is my PnL, which shows that I held this trade for about two months.

What's Next

In the next edition we'll be looking at the upcoming SpaceX, Anthropic, and OpenAI IPOs, how they might ripple into crypto markets, and whether they look worth getting into.